Global Commodity

Commodities jumped, capping the biggest monthly rally in 34 years, as the slumping dollar bolstered demand for energy, metals and crops as a hedge against inflation. The US Dollar Index, headed for its sharpest monthly drop this year, lowest level in five months against a basket of six major currencies, fell 5% on speculation that gains in equities and signs of a global economic rebound will spur demand for higher- yielding assets. Precious metals typically move inversely to the US currency. The Reuters/Jefferies CRB Index climbed as much as 13%, the most rally since July 1974, extending to the highest level since Nov. 2008.

As we approach mid-2009, the global economic outlook has shifted from one of pessimism and fear of the unknown to optimism and a feeling that the worst of the financial crisis and global recession may be behind us. The premise for the recovery in base metals prices has been based on very little evidence; however, the fact that Chinese imports of refined metal have exceeded expectations is not based on any real pick-up in consumption, but more on the shifting of surplus metal from one location to another. The main forces behind this have been Chinese consumer and State Reserves Bureau restocking, and the strong arbitrage trade in Copper, Zinc and Aluminum.

Gold and Silver

Gold jumped 9%, most for a month since November and topped $980 an ounce yesterday. Silver had the biggest monthly increase in 22 years and rocketed 30% higher in May on rising economic optimism and firm gold prices. Prices for bullion moved higher as the dollar sank to its lowest level in five months against the euro and the British pound. The dollar has weakened considerably since March as investors move out of cash holdings and into riskier assets like stocks on hopes for an economic recovery. Investors are also worried that the massive amounts of money the government has been pumping into the system could lead to inflation. That has been a boon for commodities like Gold and Oil. Demand for gold tends to rise when the dollar is weak as investors seek protection against inflation, which can be triggered by a falling greenback.

There is an extreme fear that the U.S. economy may lose its AAA credit rating in due course, and this has been feeding the gold bulls pretty well. Things really aren't improving despite the [stock] market's desire to latch on to every little bit of positive news. The reality is the economy is still struggling quite significantly. Gold holdings in the SPDR Gold Trust, the biggest exchange-traded fund backed by bullion, increased 13.14 metric tons to 1,118.76 metric tons as of May 22

Global gold hedging was unchanged in Q1 2009 from Q4 2008, the first time it had not fallen since Q1 2002. An unusual amount of new project-related hedging and an absence of dehedging from the larger hedgers were behind the stasis. India's gold imports so far in May have been in the range of 10 to 15 tonnes, lower than 29 tonnes imported in all of May of 2008 as high prices have subdued buyers' appetites.

Gold is expected to trade on an upward bias for the next month with resistance of $1000 and may touch new high crossing $1033. This rally would be sustainable if we see some retracement in prices in initial days of the month.

Zinc

Zinc has plenty to gain from the on-going Chinese and US stimulus packages and its price has risen in anticipation. However, industrial activity is about to slacken off even more during the imminent northern hemisphere summer months and this ought to see subdued price volatility, although any further mine closures could offer support. LME zinc stocks have declined, falling to about 10 days worth of consumption, while the three-month price has gained 5% since April to reach $1570/t on 29th May.

Much of the LME stock has been sucked into China to feed state and consumer restocking programmes, which in turn have opened a strong arbitrage trade between the higher Shanghai prices than that of the LME, encouraging further imports. There is little fundamentally in the short-term to keep the price at such a high level, but zinc, more than any other base metal, entered into recessionary territory almost 18 months ago and the amount of mine and smelter production cuts and closures reflects this. It is estimated; about 1.6 Mt of mined zinc production has been cut or closed and 1.4 Mt of refined zinc output in 2009. Importantly, some of the mine closures are likely to be permanent, while others will take time and require financing to restart.

With zinc standing to benefit from the Chinese infrastructure-focused stimulus package more than the other base metals, besides perhaps copper, we expect to see some tightness in the market later in 2009, as some real demand returns. For the next month, we could see some profit booking in the initial days and that would be opportunity to build long position. Zinc is likely to trade higher next month with the resistance $1640 and $1700.

Lead

Lead prices have been in thrall to copper in May, with prices trading wildly in $200/t ranges. LME three-month lead started May at lowest level at $1325/t and ended at highest level of the month at $1570/t. Besides echoing copper, lead’s price strength can be traced to a number of reasons. The normally recession-resistant replacement battery sector, which accounts for about 40% of lead offtake, has benefited from the unusually cold winter in the northern hemisphere.

In addition, it is estimated about 360,000t of lead production has been cut in 2009 due to the severe cuts by zinc miners, as Lead is produced primarily as a by-product from zinc mines. This has tightened the market considerably, leaving LME stocks at no more than three days worth of consumption. Adding to this is the fact that China has become a net importer of lead. In 2007 it exported a net 211,000t, and in 2008 a net 2,700t. In Q1 2009 it imported 48,320t of refined lead, up 826% year-on-year. Also supporting the price was the suspension of US-based Doe Run’s La Oroya lead-zinc-copper smelter in Peru, which produced 114,000t of lead in 2008. It has now restarted, albeit at reduced capacity.

Lead looks the brightest fundamentally of all the base metals besides tin. The low level of LME stocks and tightness in near-term supply will support the price over the next month. For the next month, we could see some profit booking in the initial days and that would be opportunity to build long position. Zinc is likely to trade higher next month with the resistance $1640 and $1700.

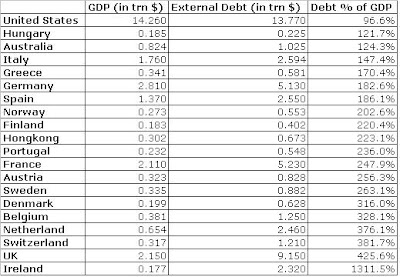

Source: External Debt (2009) information from The World Bank, GDP (2009) information from the CIA World Factbook.

Source: External Debt (2009) information from The World Bank, GDP (2009) information from the CIA World Factbook.

Ahmedabad Time

Ahmedabad Time